Are car insurance rates set by law?

Yes and no. Car insurance rates are regulated by the states, but as long as companies observe state laws, they are free to charge what they wish.

State laws ensure that a company charges the same rates to drivers who fit the same risk profile. Another company may charge you much less, or much more, but it, too, must offer same rates to all drivers who pose a similar risk.

Insurance companies are prohibited from using certain characteristics in setting their rates, such as race and religion. California, Hawaii and Massachusetts prohibit use of your credit information, and others don’t allow companies to penalize you based on your age or your gender.

All states set minimum levels of liability insuranceLiability insurance covers sums that an insured becomes legally obligated to pay because of bodily injuries or property damage, or financial losses caused to other people. coverage. Some require that you buy uninsured motorist coverage. Some make medical payments coverageAn auto insurance coverage that provides coverage for medical expenses incurred by you and your passengers in the event of an accident, regardless of who is at fault. mandatory. These financial responsibility laws ensure that drivers who inflict injuries on others have a means to pay, and those who are injured have coverage if the other driver does not.

Your lender may require that you buy comprehensive and collision coverage to protect your car from physical damage, but no state requires it.

How is car insurance calculated?

When you submit an application for car insurance, you are sorted first into an individualized group – say, married drivers in your ZIP code over age 25. Once your customized group has been determined, the insurance company calls up the pricing information for that group. It adjusts for any negative factors, such as recent traffic violations or a pattern of claims. It considers the value of the car you are insuring and the frequency of claims its owners file. Finally, any discounts you qualify for are subtracted from the price, and your quote is returned.

The math is done behind the scenes according to an algorithm that weighs each risk factor – each bit of information you or your agent enters into the system.

If you decide to buy a policy, your quote information goes through a verification process called underwriting. The company pulls your driving record and those of anyone else listed on the policy. It looks up your claims history. It matches your vehicle identification number to ensure it has the correct model. If the company finds an error, it has the right, within a certain period of time, to offer you a new rate or to cancel the policy.

Why do insurance companies have such different rates?

Each company has many different basic rate groupings and can set different prices for those groups, basing its estimate of risk on the number and cost of claims that group has filed in the past. Then the company applies its own surcharges and discounts based on factors specific to a particular driver.

That means car insurance rates can vary considerably from one company to the next.

In high-cost states, such as Michigan, California and Louisiana, the difference can be much greater. In low-cost states such as Maine or Ohio, the differences tend to be smaller.

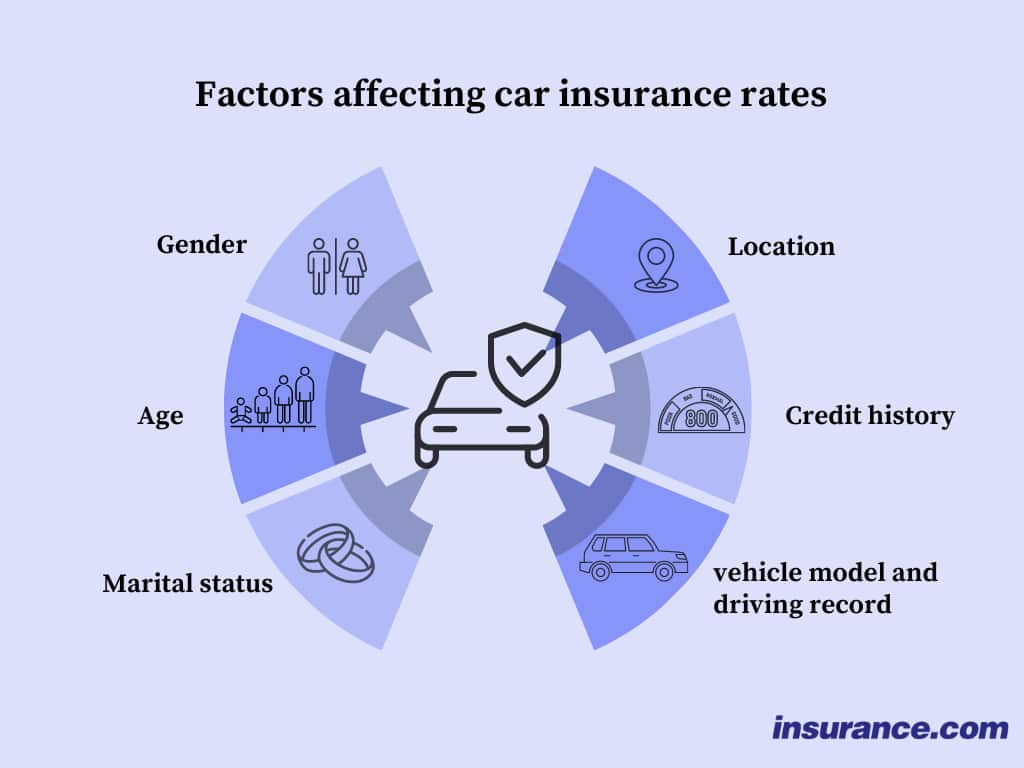

What affects the auto insurance rate quotes I receive?

Depending on state laws, which can restrict the type of information an insurance company may use, these factors will usually affect your rates:

Demographics. Age, gender, marital status, ZIP code, number of years you’ve been licensed, homeownership, occupation, education and even grades

Your record. Accidents, traffic violations, insurance history, credit history, past claims of all types

Your car and how you use it. Owned or financed, current value, annual mileage, claims record for all owners of that model, anti-theft devices and safety features, whether you use the car for business.

How much coverage you want. Liability limits, whether or not you buy comprehensive and collision (both of which carry a deductibleThe deductible is the amount you pay out of pocket for a covered loss when you file a claim. that influences their final cost), medical payments, uninsured motorist, or extras such as rental reimbursement or towing.

Which factors affect car insurance rates most?

While each car insurance company decides on its own how heavily to weigh a rating factor, clear patterns are evident. For most drivers, these factors tend to influence rates most:

Your ZIP code. Even if you have never filed a claim, your rate can increase dramatically simply by moving from one ZIP code to another.

Your age. Drivers with less than 10 years of experience pay more. The less experience you have, the worse the penalty. Brand-new drivers can pay an additional surcharge on top of that.

Your driving record. Claims tend to matter more than speeding tickets do. More than one of either is bad news, and so is a major violation such as a DUI.

Your credit. Insurance companies point to numerous studies that correlate poor credit scores with higher numbers of claims. The flip side: When your credit improves, your rates should decrease.

Your previous insurance coverage. If you are not currently insured, you are likely to pay much higher rates for at least your first term.