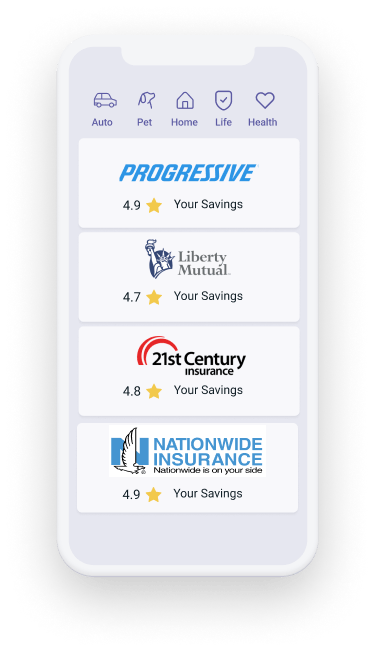

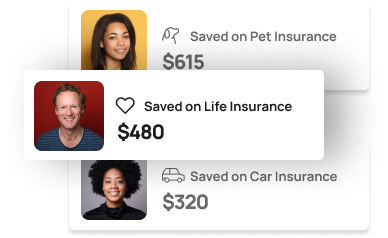

Shop smart - Compare your savings options

Your insurance needs aren't quite like anyone else's, so you need insurance rates that are calculated just for you. With just a few easy steps, you'll get insurance quotes that are tailored to your needs from the best insurance companies in the business.

The quick-start guide to shopping for insurance

Get answers to your insurance questions

Insurance 101

Calculate & compare the rates for your coverage

With just a few easy steps you can compare rates from the top insurance companies and choose the best coverage for your needs.

The latest research, the best advice

Our experts stay on top of trends, rate and rule changes, and important insurance news. Check out our latest guides and insurance explainers to get answers to all your insurance questions.

How much is full coverage insurance in 2025?

The average full coverage car insurance cost is $1,895 a year, but rates will vary depending on the insurance company you choose, where you live and other factors. Nationwide is the cheapest company for full coverage at an average rate of $1,548 a year.

Average home insurance cost: How much is home insurance in 2025?

The average cost of homeowners insurance in the U.S. is $2,601 a year, putting the average cost of home insurance per month at $217, for $300,000 in dwelling coverage. At that coverage level, Allstate is cheapest at $2,098 annually. Your insurance rate will vary based on where you live and factors specific to your home.

Average condo insurance cost in 2025

The average cost of condo insurance is $656 a year, or $55 per month. However, costs can vary depending on where you live and how much coverage you purchase. A condo insurance calculator is a useful tool for estimating rates.

What is non-owner car insurance and who needs it?

Non-owner auto insurance is liability-only car insurance for a driver who doesn’t own a vehicle but drives other people’s vehicles often. It provides additional liability insurance should you get into an accident while driving someone else's car or a rental. Non-owner car insurance is secondary, which means it kicks in when the owner's limits are exceeded.

How much is renters insurance in 2025?

You can expect to pay about $22 a month for renters insurance in the U.S. Renters insurance rates are affected more my personal property coverage than by liability. At $40,000 in personal property coverage and $100,000 liability the average cost is $246 a year; for $300,000 in liability the average annual cost is $263.

Why you can trust us

- We know every step of the insurance buying process and can provide guidance from start to finish -- whether it’s auto, home, life or any other insurance you need.

- We know the frustrations insurance customers face, from understanding the jargon on a policy to dealing with a claim. We’ve been there and we can help you navigate it.

- We want you to find the best coverage for your needs, not the coverage someone wants to sell you whether it’s right for you or not. We’re on your side, offering objective, data-based advice.

- We understand insurance right down to the smallest details, even complex purchases like health insurance, and we make it easy for you to understand.

- We bring more than 25 years in the insurance industry to help guide your insurance-buying decisions.

Get to know our team of insurance experts

Our insurance experts have decades of insurance knowledge and are dedicated to educating consumers so they can make the best decisions about their insurance coverage.